We Surveyed Families About Investing. Good Intentions Were Everywhere — Follow-Through Was Not

What if the biases shaping our kids aren't the ones we hold, but the ones we'd swear we don't? That question is what started us exploring. This month, working alongside our summer intern Ranya Patel, we surveyed American families about how they teach their children about money, and found that the gap between what parents believe and what they pass down is wider, and quieter, than anyone wants to admit.

We ran our survey as a within-family comparison: one parent answered the same questions about their son and their daughter. It's a simple design that revealed some interesting findings. When the same parent describes both children, the usual noise (e.g., income, the parent's own financial confidence, family structure) drops out. What's left is how one person treats two kids who differ mainly by gender.

Here's what surprised us. The bias wasn't in what parents believed. It was in what they did.

Ask parents about their intentions and the gap disappears. Do you encourage this child to take smart financial risks? Would you be comfortable with your child investing? Do you expect this child to be good with money? Mothers and fathers rated their daughters and sons the same.

Then, we asked what parents actually discuss. And that’s where the picture changed.

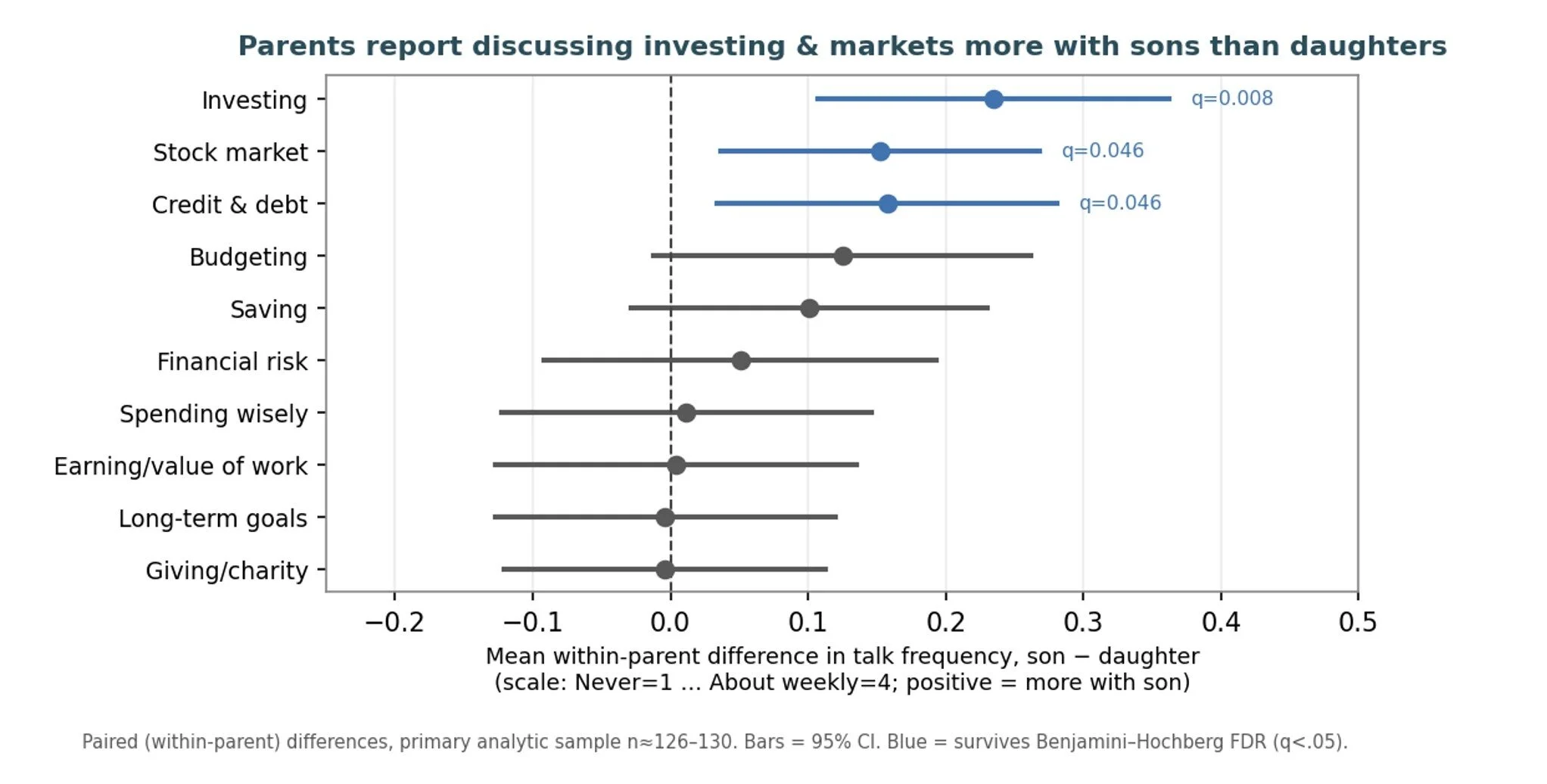

Parents reported talking about investing, the stock market, and credit and debt noticeably more often with their sons than their daughters. The clearest gap was investing and discussing the stock market.

What makes this interesting is that there wasn’t a gap on saving, spending, budgeting, earning, giving, or long-term goals. The asymmetry showed up in one cluster only: the conversations about investing (i.e., building wealth).

We pulled out the parents who told us, plainly, that they talk to their kids about money "the same way regardless of gender." Eighty percent of our sample agreed with that statement. I believe they meant it. But the investing gap held in that group anyway.

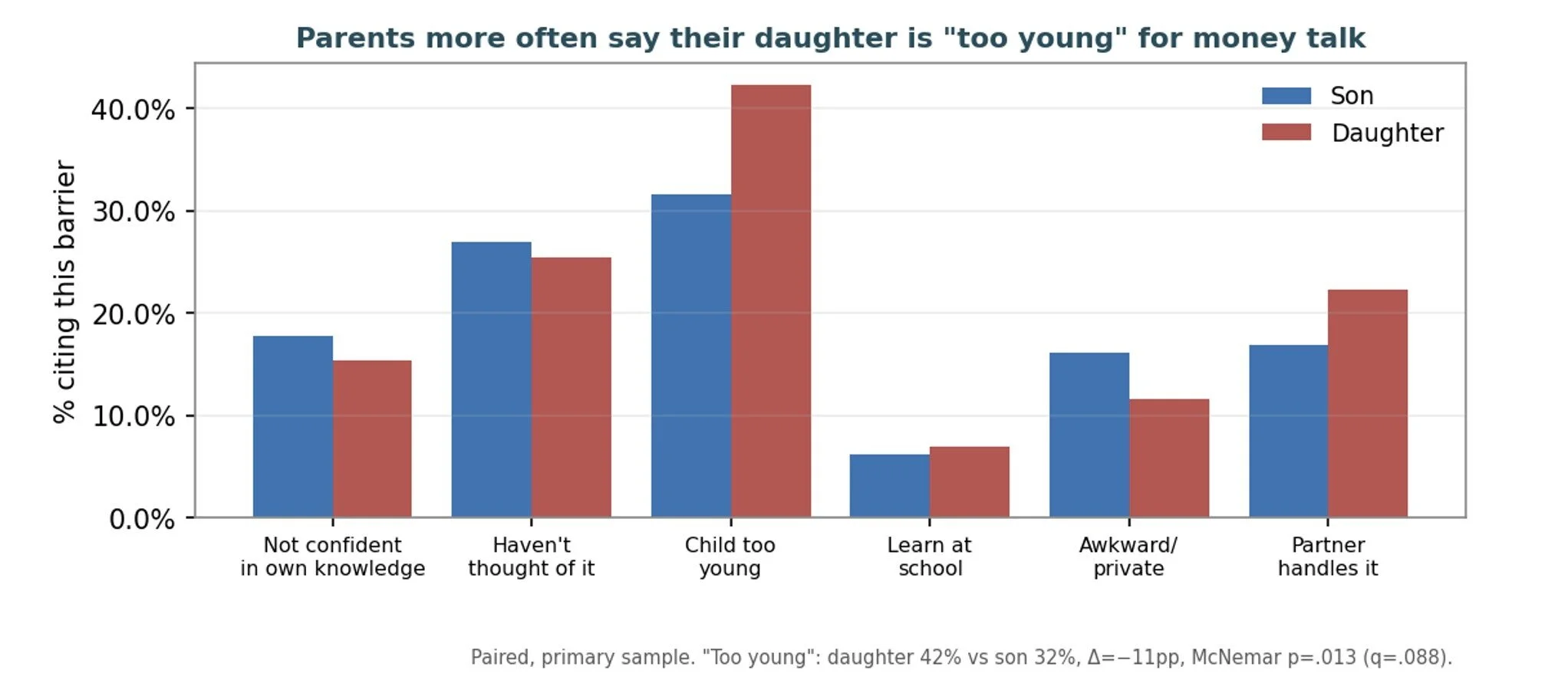

So, parents are acting against their own stated values not out of a bias they'd defend, but out of a pattern invisible to them. And when we asked what gets in the way of money conversations, one element stood out: Parents were more likely to call their daughter "too young" for the conversation than their son. Forty-two percent versus thirty-two. Same household. Same age range. Different read on readiness.

It's not that parents doubt their daughters can handle money. It's that, somewhere below awareness, sons read as ready a little sooner.

Now, you might call this trivial, but we don’t believe it is. Because this isn’t confined to the home. In The Authority Gap: Why Women Are Still Taken Less Seriously Than Men And What We Can Do About It, Mary Ann Sieghart points to research showing that by the age of six (six!) children of both genders already believe boys are more likely to be "really, really" smart than girls. That's the climate our investing conversation lands in: A deficit in confidence long before anyone even opens a brokerage account. And confidence is the whole game. A girl who doubts she's smart enough doubts she's going to be good at investing, and that doubt compounds for decades, right alongside the money she doesn't put to work.

I started Girl Gonna Launch three years ago to help build middle school girls’ confidence through entrepreneurship. Over the past year, we've been widening the lens to financial literacy, for a reason that's easy to state and hard to overstate: Time is the most powerful force in building wealth, and girls are too often introduced to it late.

A girl who starts investing at 18 has decades that compound. A woman who starts at 37 has lost that stretch of time. The wealth gap between men and women isn't only about what people earn. It's about who started building, and when. Our findings point to one quiet contributor, in a conversation that happens a little less often for the daughter.

We all understand that wealth is independence and freedom. When girls grow into women with real wealth, they have the power to fund the causes they care about, back the founders they believe in, and make the change they want to see. Investing confidence isn't the finish line, but it is a critical on ramp.

I want to be fully transparent that this was a paid online panel, not a representative sample of all American parents. Our respondents were unusually educated and unusually confident about money, so these numbers describe this group, not the country as a whole. The effects are small. The data comes from one parent's self-report, with no second voice in the room to check it. We didn't capture each child's exact age, which means a sliver of the investing gap could reflect sons being the older sibling rather than gender itself.

If the gap is just about airtime (i.e., who gets pulled into the conversation about markets and investing) then the fix isn't actually that hard. We don't have to change what parents believe, or what society believes. We just have to change who gets invited in; who gets access to the information, and the encouragement. And that's something we can do in a classroom: Put the investing conversation in front of middle and high school girls.

This survey was designed and run with our summer intern, Ranya Patel, whose curiosity shaped every part of it. Watching a young woman lead research on the exact gap we're trying to close is its own kind of answer to the question.

If you work in financial education or research design or you're a parent of middle school girls, we'd love to hear from you…